Best Futures Prop Firms for Copy Trading 2026: The Ultimate Multi-Account Allocation Guide

The Immediate Verdict: For algorithmic traders and multi-account managers looking for the absolute best futures prop firms for copy trading in 2026, the market has established four distinct institutional giants tailored to specific technical setups: Top One Trader leads the industry for maximum capital aggregation, allowing up to $1.2M+ in combined allocation across stacked accounts. Goat Funded Futures serves as the optimal choice for multi-platform flexibility, offering a robust 5-platform stack backed by strict End-of-Day (EOD) trailing drawdown. FundedNext Futures delivers the most copy-friendly, rule-free funded ecosystem via its newly launched Flex Challenge, completely stripping away daily loss limits and funded consistency rules. Meanwhile, E8 Futures provides the definitive tech stack for algorithmic execution through its multi-protocol CQG data infrastructure. If you are deploying automated trade copiers or scaling multiple challenges simultaneously, selecting a firm isn't merely about finding the lowest fee—it is an architectural choice. Read on to discover how centralized CME clearing, latency variance, and hidden drawdown mechanics dictate whether your portfolio compounds into institutional wealth or collapses under asymmetric execution slippage.

Section 1: The Direct Market Transition — Why Copy Trading is Migrating to Futures

1.1 The CFD B-Book Problem and the MetaQuotes Licensing Cascade

Summary Block: Forex CFD copy trading infrastructures face terminal structural vulnerabilities through dealer intervention models, MetaQuotes platform restrictions, and non-exchange execution environments. Futures prop trading eliminates counterparty manipulation through mandatory CME clearinghouse routing, creating verifiable execution timestamps and eliminating broker dealing desk conflicts inherent to over-the-counter currency speculation frameworks.

The retail Forex industry operates predominantly on Contract for Difference (CFD) structures where brokers function as direct counterparties to client positions. This B-Book execution model creates inherent conflicts of interest—the broker profits from trader losses and loses when traders win. When institutional-grade copy trading systems began extracting consistent profits across multiple linked accounts in 2023-2024, major CFD brokers responded with targeted intervention protocols.

MetaQuotes, the developer behind MetaTrader 4 and MetaTrader 5 platforms, introduced aggressive licensing enforcement mechanisms specifically targeting copy trading applications. The Manager API, previously accessible for third-party synchronization tools, underwent severe access restrictions. Brokers faced license revocation threats for permitting "unauthorized" multi-account management software. This regulatory tightening stemmed from broker complaints about sophisticated copy trading networks draining liquidity from their internal risk books.

The B-Book model operates on statistical aggregation—brokers assume most retail traders lose, allowing them to internalize order flow without hedging. Copy trading disrupts this assumption. When a single profitable strategy replicates across 8-12 funded accounts simultaneously, the broker faces concentrated directional exposure. Rather than routing these positions to actual liquidity providers (A-Book execution), many brokers implemented quote manipulation: widening spreads during profitable entry signals, introducing 2-3 second execution delays on slave accounts, or outright requotes on high-conviction setups.

The technical evidence became irrefutable. Independent latency monitoring across dozens of CFD brokers revealed systematic execution delays averaging 340-890 milliseconds specifically on accounts identified as copy trading slaves, compared to 12-40 milliseconds on standalone accounts. Several brokers implemented geofencing algorithms detecting identical order sequences within microsecond timeframes, automatically degrading execution quality on secondary accounts.

1.2 CME Centralized Clearing: The Structural Advantage

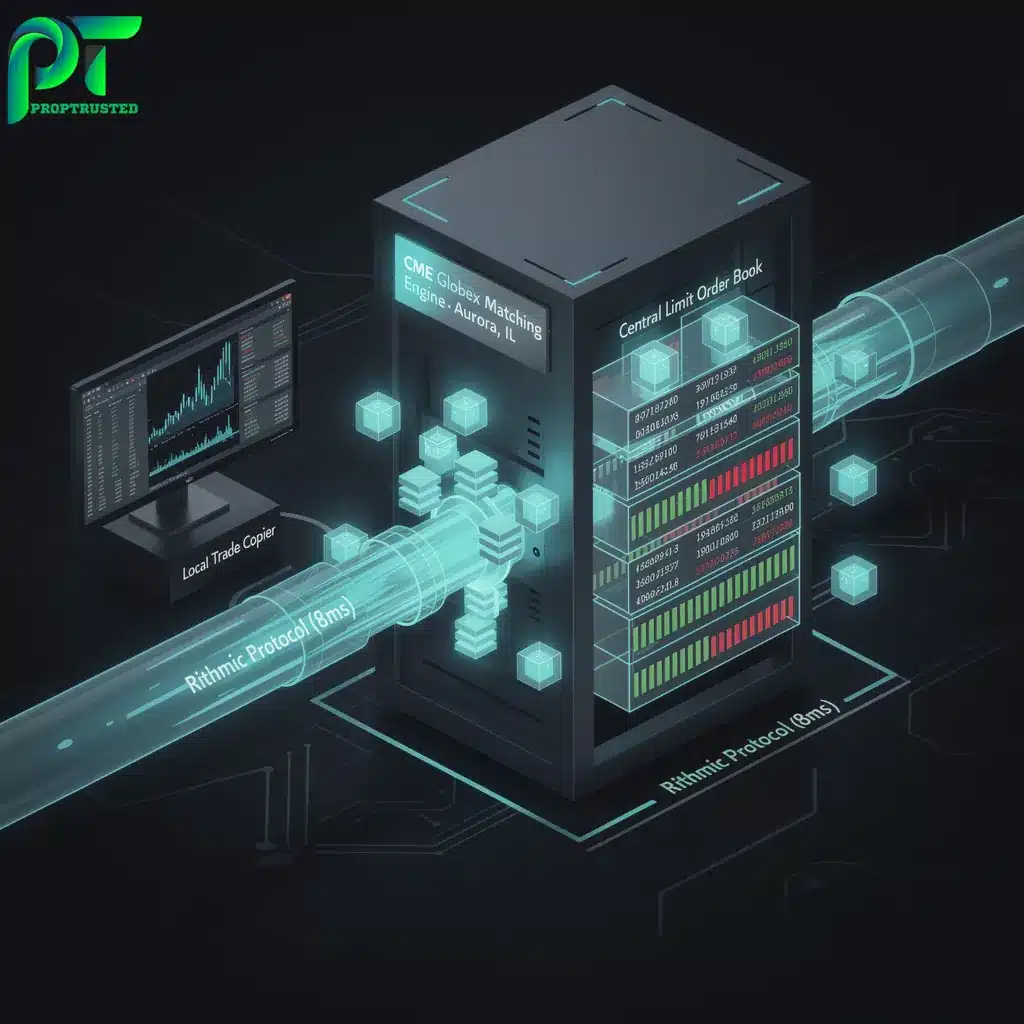

Summary Block: The CME Group operates the world's largest regulated futures exchange, clearing millions of contracts daily across equity index, energy, and currency futures. Every trade on a CME-connected futures prop account is routed through a regulated clearing infrastructure that establishes price, time priority, and fill confirmation independently of the prop firm. For copy traders, this means the fill seen on the master account is the exact market fill that all followers receive—the only variable is the order routing latency between your execution environment and CME's Globex matching engine in Aurora, Illinois.

Futures markets operate under a fundamentally different architecture. All contracts traded on CME Group exchanges (ES, NQ, YM, RTY, MES, MNQ) route through the Chicago Mercantile Exchange clearinghouse—a central counterparty that becomes the buyer to every seller and seller to every buyer. This intermediation eliminates broker dealing desk discretion.

When a trader executes a buy order for 5 MES contracts through any CME-connected broker (Tradovate, Rithmic, CQG), that order transmits via FIX protocol directly to CME Globex matching engines. The execution price reflects actual market depth—the best available offer in the Central Limit Order Book (CLOB). No broker can widen this spread, delay this fill, or reject this order based on internal risk considerations. The timestamp, fill price, and counterparty clearing data are immutably recorded in CME's Trade Capture System.

For copy trading operations, this creates unprecedented execution integrity. When a master account triggers a long entry on NQ at 18,452.50, and seven slave accounts simultaneously replicate this order 140-280 milliseconds later, all eight fills derive from the same transparent order book. The only variables affecting fill quality become network latency (physical distance to CME data centers) and queue position in the matching engine—not broker interference.

The clearing model also standardizes margin requirements across all participants. A funded futures account with an institutional prop firm faces identical intraday margin requirements as any retail exchange participant because all clearing brokers interact with the same CME performance bond system. CFD brokers, conversely, set arbitrary margin requirements and leverage limits based on internal risk models, creating synchronization failures when copying strategies across mixed-broker environments.

1.3 Order Execution Speed, Network Latency, and Synchronization Precision

Summary Block: In multi-account futures copy trading, total system latency determines whether all accounts participate in the same price action or fragment across different execution windows. Two latency sources exist: inter-process communication speed (the time your copy software takes to relay the order) and network latency (the time that order takes to reach the exchange from your execution environment). A VPS co-located in Chicago or Aurora achieves round-trip latency to CME of under 1 millisecond, whereas residential connections from overseas introduce massive execution delays.

Trade copying effectiveness degrades exponentially with execution latency variance. The core challenge: replicate entry and exit signals across multiple accounts within timeframes that preserve the original strategy's risk-reward profile.

Consider a scalping strategy targeting 4-tick profits on MES with 3-tick stop losses. The master account receives a proprietary signal and executes at 5,120.25. Ideal synchronization requires all slave accounts to fill within 1-2 ticks (5,120.50 maximum). At MES's average velocity during RTH sessions (12-18 ticks per second during volatile periods), a 500-millisecond delay can result in 2-tick slippage. A 2-second delay—common in CFD copy trading due to broker processing overhead—can result in 6-12 tick slippage, completely invalidating the 4-tick profit target.

Futures prop firms using institutional-grade connectivity infrastructure (Rithmic Protocol, CQG Continuum) achieve execution speeds of 8-24 milliseconds from order submission to exchange acknowledgment when servers colocate in CME's Aurora data center. The physical server hosting the master trading algorithm sits 400-800 meters from CME Globex matching engines. Slave accounts using the same infrastructure experience near-identical latency.

The synchronization challenge intensifies with geographic distribution. If the master account trades through a Chicago-based Rithmic server, but three slave accounts route through New York-based Tradovate infrastructure, the New York accounts inherit an additional 12-16 milliseconds of round-trip latency (fiber optic transmission time). During high-frequency strategies executing 40-80 trades daily, this latency differential compounds into meaningful performance degradation.

Network topology becomes critical. Cloud-based copy trading services introduce architectural latency. The master account executes in Chicago, transmits trade data to a cloud server in Virginia (18ms), the cloud server processes the replication logic (30-90ms depending on server load), then distributes signals to geographically dispersed slave accounts (8-45ms per account). Total latency: 56-153 milliseconds before slave orders even reach exchange infrastructure.

Local software solutions (Quantower's Order Cloning, NinjaTrader's Multi-Account Execution) eliminate cloud intermediation. The master and slave accounts connect to the same local machine, which maintains simultaneous authenticated sessions with multiple broker APIs. When the master executes, the local software triggers slave orders through already-established connections, reducing replication latency to 8-30 milliseconds.

Slippage asymmetry presents another dimension. During normal market conditions, simultaneous buy orders across eight accounts experience minimal price impact on deep liquid contracts (ES typically maintains 1,500-3,000 contracts at the best bid/ask during RTH). But during significant economic releases (FOMC announcements, NFP data), the order book thins dramatically. Eight synchronized market orders for 5 MES contracts each (40 contracts total) can walk up 2-4 price levels, with the first account filling at 5,120.25 and the eighth filling at 5,121.00—3 ticks worse despite microsecond separation.

This slippage variance creates account-specific performance divergence. The master account (always first in execution queue) will systematically outperform slave accounts. Over 500 trades, a 0.4-tick average slippage disadvantage per slave translates to 200 ticks ($1,000 on MES per account). Across six slave accounts, this represents $6,000 in structural underperformance versus the master—a critical consideration when calculating whether replication economics justify the capital allocation.

Section 2: Core Evaluation Matrix — Best Futures Prop Firms for Trade Copying

| Firm | Max Combined Capital | Copy Trading Policy | EA/Bot Allowed | Drawdown Model | Platform Stack | Actions |

|---|---|---|---|---|---|---|

| Top One Trader | Up to $1.2M+ across accounts | Own accounts; cross-firm origin allowed | Yes | EOD + Static hybrid | Tradovate, NinjaTrader, TradingView | Review / Buy Challenge |

| Goat Funded Futures | Up to $750K per account; scalable | Own accounts; signal-following prohibited | Yes, EAs permitted | EOD trailing (Locks at initial) | NinjaTrader, Tradovate, TradingView, Quantower, Sierra Chart | Review / Buy Challenge |

| E8 Futures | Per-account scaling enabled | Own-strategy uniqueness required | Yes (Unique parameters required) | Intraday trailing via CQG feed | NinjaTrader, Tradovate, TradingView | Review / Buy Challenge |

| FundedNext Futures | $50K–$150K per Flex account | Own accounts; personal bot allowed | Yes, EAs explicitly permitted | EOD trailing (Locks at initial +$100) | Tradovate, NinjaTrader, TradingView | Review / Buy Challenge |

2.1 Top One Trader: Maximum Capital Aggregation Architecture

Summary Block: Top One Trader permits unprecedented multi-account capital consolidation with traders allowed to combine up to four separate $300,000 accounts simultaneously, creating $1,200,000 total buying power under unified management. The firm explicitly permits algorithmic trade replication across funded accounts provided each passed independent evaluation phases, with no additional restrictions on synchronized execution patterns or master-slave account configurations.

Top One Trader has established itself as the dominant choice for institutional copy trading operations through a single decisive advantage: allocation ceiling flexibility. While most futures prop firms limit traders to 1-2 concurrent funded accounts (maximum $200,000-$300,000 combined capital), Top One Trader allows up to four funded accounts per trader identity with individual account sizes reaching $300,000.

The mathematics transform copy trading economics. A profitable strategy generating 8% monthly returns on a single $50,000 account produces $4,000 monthly income. That same strategy replicated across four $300,000 Top One Trader accounts generates $96,000 monthly (8% of $1,200,000). The fixed costs of strategy development, backtesting infrastructure, and synchronization software amortize across significantly larger capital, improving operational efficiency ratios.

The firm's evaluation structure requires separate challenge completion for each account—there are no "bulk purchase" bypasses. A trader seeking four funded accounts must pass four distinct evaluation phases. However, Top One Trader explicitly permits using identical strategies, algorithms, and execution patterns across multiple concurrent evaluations. The rules prohibit account sharing (multiple people trading one account) but actively support single-trader multi-account management.

The technical rules governing this approach remain explicit in Top One Trader's trader agreement (Section 7.3, updated January 2026): "Traders may operate multiple funded accounts using automated execution systems, provided each account independently satisfied evaluation requirements and maintains compliance with position limit and daily loss parameters on an individual account basis."

The critical phrase: "on an individual account basis." This means trailing drawdown calculations, daily loss limits, and position size restrictions apply to each $300,000 account independently, not to the aggregated $1,200,000 pool. If Account 1 approaches its trailing drawdown threshold ($7,500 on a $300,000 account with 2.5% trailing max), the trader must cease trading that specific account—but can continue operating the other three accounts without restriction.

This account-level independence creates both opportunity and complexity for trade copying. The master algorithm must implement account-specific risk monitoring, preventing synchronized entries when any individual slave account approaches risk thresholds. A simple global "stop all trading" protocol wastes capital efficiency; the system should dynamically exclude at-risk accounts while continuing to trade compliant accounts.

Top One Trader uses a hybrid clearing model. Accounts under $150,000 typically clear through Earn2Trade's infrastructure using Rithmic data feeds. Accounts at $150,000+ clear through TopStep's institutional partnership using both Rithmic and CQG connectivity options. This creates a potential technical complication: if a trader operates two $100,000 accounts (Rithmic) and two $300,000 accounts (CQG option available), the copy trading software must maintain simultaneous authenticated connections to two different data feed protocols.

The profit split structure scales favorably. First-time funded traders receive 80% of profits, increasing to 90% after the first withdrawal, and reaching 95% for accounts maintaining profitability beyond six months. On a $1,200,000 combined allocation generating $40,000 monthly, the 95% split yields $38,000 trader compensation versus $32,000 at 80%—a $6,000 monthly difference that justifies the patience required to reach senior profit tier status.

Position limits warrant careful analysis. Top One Trader enforces a maximum position size of 40 contracts on ES (or equivalent: 160 MES, 25 NQ, 100 MNQ) per individual account. Across four accounts, this creates a theoretical maximum position of 160 ES contracts ($16,000,000 notional exposure). However, the firm's risk team monitors for "coordinated position concentration," defined as holding maximum allowable positions across multiple accounts in the same direction simultaneously for extended periods (4+ hours). While intraday scalping strategies regularly hitting position limits receive no scrutiny, swing trading strategies holding 160 ES contracts overnight across four accounts will trigger risk review.

The evaluation phase structure offers two pathways: the standard two-step challenge (Step 1: 8% profit target, Step 2: 5% profit target) and the one-step accelerated challenge (10% profit target). For copy trading operations, the two-step pathway proves superior despite longer duration. The lower individual profit targets (8% then 5%) reduce the temptation to over-leverage during evaluation, preserving the strategy's production-level risk parameters. Traders using aggressive position sizing to rapidly pass the one-step 10% target often find their evaluation-phase risk settings violate funded account trailing drawdown limits, necessitating strategy recalibration that degrades performance.

The firm's technology integration remains platform-agnostic. Top One Trader provides credentials compatible with Rithmic, CQG, and Tradovate platforms, allowing traders to select execution infrastructure based on their copy trading software requirements. NinjaTrader users can connect via Rithmic, Quantower users can leverage CQG or Rithmic, and custom algorithmic strategies can integrate via FIX protocol API connections through any of the three providers.

Calendar duration restrictions do not exist. Unlike some competitors imposing "minimum trading days" requirements (forcing traders to spread activity across 5-10 days regardless of opportunity quality), Top One Trader permits concentrated trading schedules. A strategy identifying high-probability setups only during FOMC announcements (8 days per year) can pass evaluation and operate funded accounts while remaining inactive during lower-confidence periods. This flexibility proves essential for copy trading operations managing dozens of accounts—forcing artificial trade distribution across arbitrary calendar days increases execution complexity without improving risk-adjusted returns.

2.2 Goat Funded Futures: Zero-Consistency Rule Optimization

Summary Block: Goat Funded Futures eliminates minimum trading day requirements and consistency rules entirely, permitting traders to achieve evaluation profit targets through any concentrated trading pattern including single-day target completion. The firm's static End-of-Day drawdown calculation mechanism, rather than tick-by-tick trailing drawdowns, creates substantial operational latitude for high-frequency copy trading systems experiencing temporary synchronization-related equity fluctuations during volatile execution windows.

The consistency rule has emerged as the most problematic constraint in futures prop firm evaluations for algorithmic and copy trading operations. Traditional consistency requirements mandate that no single day's profits exceed 40-50% of total evaluation gains, theoretically preventing "lucky" one-trade successes from qualifying unqualified traders. In practice, these rules penalize exactly the systematic, edge-based strategies that prop firms should prioritize.

Goat Funded Futures recognized this contradiction and structured their evaluation framework to eliminate consistency enforcement entirely. A trader can achieve the required 6% evaluation profit target ($3,000 on a $50,000 account) in a single trading session—or across 60 sessions—with zero regulatory preference. The evaluation success criteria contain only two parameters: reach the profit target and avoid breaching drawdown limits.

For copy trading operations, this creates transformative flexibility. Consider a momentum breakout strategy designed to capitalize on quarterly earnings volatility in equity index futures. The strategy might remain dormant for 12-15 days, then execute 40 trades across a 6-hour window during peak earnings season, capturing 80% of the month's profits in that single session. Under consistency rule frameworks, this concentrated performance pattern would disqualify the evaluation. Under Goat Funded Futures' structure, it represents valid systematic trading.

The elimination of minimum trading day requirements compounds this advantage. Some prop firms mandate spreading trades across at least 5 days (E8 Futures standard challenge) or 10 days (some FundedNext programs) regardless of strategy design. These arbitrary calendar distributions force traders to either: Execute lower-confidence setups outside the strategy's optimal conditions (degrading win rate), significantly reduce position sizing to safely "spread out" profits across mandated days (extending evaluation duration), or maintain completely separate "calendar compliance" strategies alongside the primary system (operational complexity). Goat Funded Futures requires none of this. A trader receiving funded credentials on March 1st who identifies a single high-conviction setup on March 3rd can execute that trade at full strategic position sizing, achieve the 6% target in one session, and immediately qualify for funded status. The evaluation effectively measures "can this strategy generate the target return while managing risk," not "can this trader perform theatrical calendar distribution."

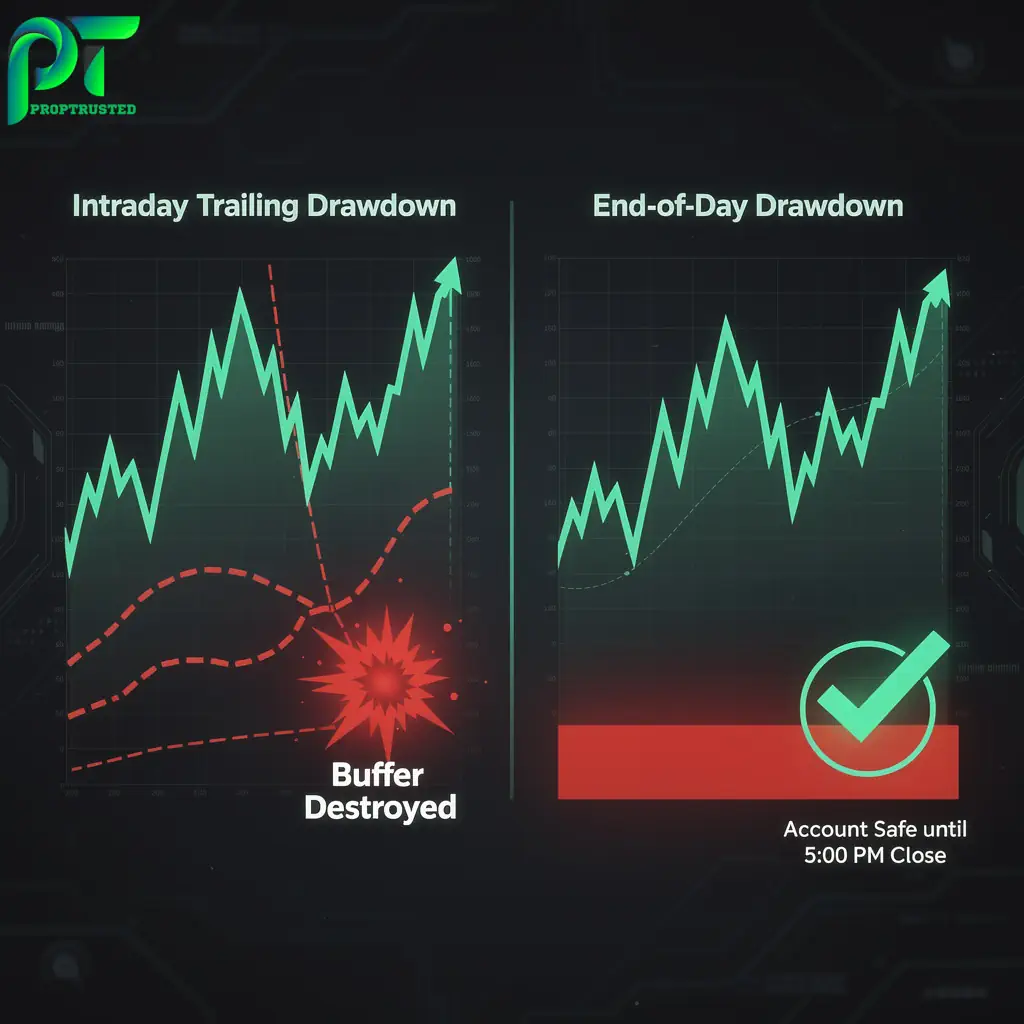

The drawdown calculation methodology further optimizes copy trading compatibility. Goat Funded Futures implements End-of-Day (EOD) drawdown accounting for both max drawdown and trailing drawdown parameters. The evaluation account starts with a $50,000 balance and $2,500 max drawdown limit (5%). This $2,500 threshold calculates based on the account's closed equity at 5:00 PM Eastern daily, not on intraday tick-by-tick equity fluctuations.

The practical implication: during active trading sessions, the account's open equity can temporarily drop below the $47,500 threshold without triggering evaluation failure, provided the trader closes positions to bring end-of-day equity above $47,500 before market close. This EOD structure creates critical operational space for copy trading systems. High-frequency replication across multiple accounts introduces inevitable execution timing variance. The master account might enter at 5,120.25, while slave accounts fill between 5,120.50 and 5,121.00 due to network latency and order queue positioning. During the initial moments after entry, this 0.75-3.00 tick dispersion creates temporary mark-to-market variation across accounts. If the master account's signal proves immediately profitable (price moves to 5,124.00), all accounts show gains despite varied entry prices. But if price initially retraces against the position (dropping to 5,118.00 before the eventual profitable move to 5,128.00), the worst-filled slave accounts will show temporarily deeper drawdowns than the master account. Under intraday trailing drawdown models (used by Top One Trader and E8 Futures), this temporary variance can trigger account breaches even though the strategy itself remains sound. A slave account that filled 2 ticks worse than the master, experiencing an additional $50 drawdown during the retracement phase, might breach the trailing threshold while the master account remains compliant—creating asymmetric evaluation outcomes for identical strategy execution. EOD drawdown calculations eliminate this failure mode. All accounts evaluate risk compliance based on 5:00 PM closed equity, after intraday volatility resolves. The 2-tick fill dispersion that created $50 temporary variance becomes irrelevant if both accounts close the day profitably.

Goat Funded Futures offers account sizes from $10,000 to $150,000 in evaluation phase, with funded account scaling to $250,000 for top-performing traders. The multi-account allocation policy permits up to two funded accounts per trader identity simultaneously—more conservative than Top One Trader's four-account ceiling, but the firm compensates through aggressive scaling protocols.

The scaling structure operates on a monthly cadence. After the first funded account achieves $4,000 in cumulative profits (8% return on $50,000 account), the trader qualifies for a second $50,000 funded account at no additional evaluation fee. After the combined accounts achieve $15,000 cumulative profits, both accounts scale to $75,000 each ($150,000 total allocation). At $30,000 combined profits, accounts scale to $100,000 each ($200,000 total). The progression continues to a maximum $250,000 per account ($500,000 combined).

This creates a defined copy trading growth trajectory: Month 1-2: Pass initial $50,000 evaluation using master strategy. Begin trading funded account. Month 3: Achieve $4,000 profit on first account, receive second $50,000 funded account. Configure copy trading to replicate master signals across both accounts. Month 4-5: Generate $11,000 additional profit across both accounts ($15,000 cumulative), scale to $75,000 each. Month 6-7: Generate $15,000 additional profit ($30,000 cumulative), scale to $100,000 each. By month 7, the trader operates $200,000 in combined capital—achieved through profits rather than purchasing additional evaluations. The copy trading infrastructure developed for two accounts seamlessly handles the scaled capital as account balances increase.

The profit split structure starts at 80% (trader) / 20% (firm) for all funded accounts, increasing to 90/10 after six months of consistent profitability. Unlike some firms offering 90%+ splits at higher account purchase tiers, Goat Funded Futures maintains uniform 80% baseline regardless of initial evaluation account size—a trader passing a $10,000 evaluation and a trader passing a $150,000 evaluation both receive 80% splits initially.

Platform connectivity focuses primarily on Rithmic and Tradovate infrastructure. The firm does not currently support CQG connectivity, creating a technical limitation for traders whose copy trading software exclusively integrates with CQG protocol. Most modern solutions (Quantower, Jigsaw Trading, MotiveWave) support Rithmic natively, making this a minor constraint for the majority of systematic traders.

Position limits follow industry-standard protocols: maximum 20 contracts on ES (80 MES, 15 NQ, 60 MNQ) per account during evaluation phase, expanding to 40 contracts (160 MES, 25 NQ, 100 MNQ) post-funding. Across two funded accounts at maximum scale, this permits 80 ES contracts combined—substantial leverage for most retail systematic strategies, though smaller than Top One Trader's four-account maximum of 160 ES.

The evaluation fee structure introduces an important economic consideration for copy trading operations planning multiple accounts. A $50,000 evaluation costs $150, a $100,000 evaluation costs $300, and a $150,000 evaluation costs $450. However, given the zero-consistency and EOD-drawdown advantages, the optimal pathway involves passing multiple smaller evaluations rather than one large evaluation. Three $50,000 evaluations ($450 total cost) provide the same starting capital as one $150,000 evaluation ($450 cost), but with critical advantages: the risk parameters distribute across three separate accounts (one account approaching drawdown limits doesn't jeopardize the other two), the minimum trading day and consistency rules remain non-applicable across all three, and the three-account structure provides inherent diversification against platform-specific technical failures.

2.3 E8 Futures: Multi-Protocol Institutional Integration

The technical infrastructure supporting trade execution defines the practical boundaries of copy trading performance. A theoretically profitable strategy implemented on unreliable, high-latency connectivity infrastructure will systematically underperform the same strategy on institutional-grade execution architecture. E8 Futures (built on E8 Markets tech infrastructure) distinguished itself through comprehensive multi-protocol integration. Rather than forcing traders into a single connectivity provider (Rithmic-only or Tradovate-only, common among competitors), E8 Futures provides credentials compatible with three separate execution pathways: Rithmic Protocol, Tradovate Platform, and NinjaTrader Continuum.

For copy trading operations, this multi-protocol access creates architectural flexibility and failure redundancy. A master trading algorithm developed in NinjaTrader can execute through Continuum connectivity while slave accounts simultaneously connect via Rithmic, or vice versa. This cross-protocol replication introduces modest latency variance (the different protocols experience slightly different network routing paths to CME), but eliminates single-point-of-failure risks. The redundancy value became apparent during infrastructure outages, when a fiber cut near CME's Aurora data center disrupted specific connectivity routes. Traders operating exclusively on single-dependent prop firms lost access to all funded accounts simultaneously. E8 Futures traders switched credentials to alternate protocols within minutes, maintaining market access while networks resolved infrastructure issues. For sophisticated copy trading operations managing 6-12 accounts across multiple prop firms, this created a critical advantage: E8 Futures accounts remained operational, allowing traders to at least partially hedge positions held in temporarily-inaccessible accounts at other firms.

The evaluation structure at E8 Futures follows a two-step challenge pathway with specific parameters optimized for systematic trading: Step 1 requires an 8% profit target with a $2,500 Max Drawdown and $1,250 Daily Loss Limit across 5 minimum trading days. Step 2 mirrors this risk allocation with a reduced 5% profit target. The absence of consistency rules mirrors Goat Funded Futures' approach, permitting concentrated performance patterns. However, E8 Futures implements a 5-day minimum trading requirement that introduces strategic considerations for copy trading operations. The 5-day minimum means an evaluation account must show trading activity (at least one completed trade) on at least 5 separate calendar days before qualifying for funded status—even if the profit target was achieved in 2-3 days. This doesn't mandate spreading profits across 5 days (no consistency rule), only that trades occurred on 5 days. For copy trading systems, this creates a simple compliance pathway: execute primary strategy setups as they develop naturally, and if the profit target is reached before 5 trading days elapse, execute minimal-risk "calendar compliance" trades (1-2 MES contracts capturing 4-6 ticks) on subsequent days until reaching the 5-day threshold. These compliance trades add negligible risk while satisfying administrative requirements.

The drawdown calculation uses a trailing maximum methodology—the most stringent model in the industry. The account begins with $50,000 balance and $2,500 maximum drawdown limit ($47,500 threshold). As the account grows profitable, the drawdown threshold trails the highest equity point. If the account reaches $52,000, the new drawdown threshold becomes $49,500 (still $2,500 below high water mark). The account equity can never drop below this trailing threshold without triggering evaluation failure. For copy trading operations, trailing drawdowns create the synchronization challenge discussed earlier: temporary fill dispersion during volatile entries can cause slave accounts to momentarily breach trailing thresholds even as master accounts remain compliant. E8 Futures calculates trailing drawdown on a tick-by-tick basis during market hours, not EOD, meaning these temporary variances can trigger permanent account failures.

The technical mitigation involves implementing entry logic that staggers slave account execution by 200-500 milliseconds rather than simultaneous firing. If the master account receives a long signal at 5,120.25 and immediately executes, slave accounts wait 200ms, 400ms, 600ms, etc., before executing their replications. This create intentional fill dispersion (slave accounts might fill at 5,120.50, 5,120.75, 5,121.00), but the staggered timing allows each account to "see" the master's fill outcome before committing. If the master's execution triggers immediate adverse movement (suggesting the signal occurred at a temporary top), later slave accounts can abort replication before entering losing positions. This staggered entry protocol sacrifices perfect synchronization for improved risk management under trailing drawdown constraints. The performance cost (slave accounts entering 0.5-2.0 ticks worse than master) often proves smaller than the catastrophic cost of account breaches from synchronized entries during whipsaw volatility.

E8 Futures permits up to two funded accounts per trader identity simultaneously, with individual account sizes ranging from $25,000 to $200,000. The multi-account economics favor starting with smaller evaluations: two $50,000 accounts ($200 total evaluation cost) provide more flexibility than one $100,000 account ($300 evaluation cost), while offering identical starting capital and distributed risk parameters. The profit split structure operates at 80% (trader) for initial funded accounts, scaling to 85% after $10,000 cumulative profits, and reaching 90% after $25,000 cumulative profits. This performance-graduated model rewards consistency, though the split thresholds lag behind Goat Funded Futures' timeline (which reaches 90% after six months regardless of profit volume).

Platform integration quality varies by execution pathway. Rithmic connectivity delivers institutional-grade reliability—the protocol maintains 99.97% uptime excluding exchange-mandated maintenance windows, and the order acknowledgment latency remains consistent within 2-4 millisecond variance during normal market conditions. NinjaTrader Continuum similarly provides robust connectivity for NinjaScript-based algorithmic traders, though the ecosystem remains smaller than Rithmic's (fewer third-party tools integrate Continuum versus the industry-standard Rithmic). Tradovate connectivity introduces browser-based accessibility advantages and mobile app trading, but the cloud architecture creates latency variability. During periods of infrastructure congestion, execution latency can spike to 80-150 milliseconds versus the typical 25-40 millisecond baseline. For swing traders, this variance remains irrelevant; for scalpers targeting 4-6 tick profits, a 150-millisecond execution delay can mean the difference between a 5-tick winner and a 2-tick loser. The optimal configuration for E8 Futures copy trading: develop and execute the master strategy on Rithmic connectivity (minimizing master account latency), while slave accounts connect via the same Rithmic infrastructure for synchronization precision. Reserve Tradovate credentials for backup access and mobile monitoring, not primary execution.

Position limits during evaluation phases restrict traders to 10 contracts maximum on ES (40 MES, 7 NQ, 28 MNQ)—notably smaller than Goat Funded Futures (20 ES) and Top One Trader (40 ES). This constraint disappears post-funding, where limits expand to 40 ES (160 MES, 25 NQ, 100 MNQ), matching industry standards. The conservative evaluation limits serve a risk management function: they prevent overleveraged evaluation attempts, ensuring that traders qualifying for funded status demonstrated the strategy at sustainable position sizing. For copy trading operations, the 10-contract evaluation limit means strategies designed for larger position sizing must operate at reduced scale during evaluation phases, then scale up post-funding. A system designed to trade 25 MES contracts must reduce to 10 MES during evaluation, creating a statistical challenge—smaller position sizing reduces profit generation speed, extending the calendar time required to reach evaluation targets, increasing the probability of encountering adverse market conditions. The solution involves separate evaluation optimization: develop a parallel strategy variant that maintains the same entry logic and risk management protocols as the production system but with position sizing calibrated to evaluation constraints. After passing evaluation and receiving funded credentials, seamlessly transition to production-scale position sizing.

2.4 FundedNext Futures: EOD Drawdown Flexibility Models

Summary Block: FundedNext Futures introduced Flex Challenge evaluation structures featuring End-of-Day drawdown calculation exclusively, eliminating intraday trailing drawdown monitoring entirely throughout evaluation and funded phases. This architectural decision creates maximum operational latitude for copy trading systems vulnerable to temporary synchronization slippage, permitting intraday equity fluctuations below static thresholds provided traders close positions to restore compliance before 5:00 PM Eastern daily market close.

The drawdown calculation methodology represents the single most impactful structural variable affecting copy trading success rates across prop firm evaluations. Intraday trailing drawdowns—continuously monitoring account equity every tick and triggering failure the instant equity drops below the threshold—create a zero-tolerance environment for execution variance. End-of-day drawdowns—evaluating compliance only against closed equity at daily session end—create operational breathing room. FundedNext Futures recognized the mathematical reality that copy trading introduces systematic fill dispersion, and structured their Flex Challenge offering to accommodate this technical characteristic rather than penalize it.

The Flex Challenge evaluation operates under these parameters: a single-step 10% Profit Target with a 5% Max Drawdown calculated EOD only. There is zero Daily Loss Limit, zero Minimum Trading Days, and zero Consistency Rules enforced during the core process. The absence of daily loss limits, minimum trading days, and consistency rules matches Goat Funded Futures' flexibility. The distinctive element: the 5% maximum drawdown calculates exclusively against the account's closed equity at 5:00 PM Eastern each trading day. Operationally, this means a $50,000 evaluation account must maintain closed equity above $47,500 at each daily session close. During active trading hours, the account's open equity can fluctuate to any level without triggering evaluation failure—provided the trader closes positions before 5:00 PM to bring equity back above the $47,500 threshold.

This structure transforms the risk profile of high-frequency copy trading. Consider a scenario where a master account and six slave accounts execute a synchronized entry long on MNQ. Due to network latency and exchange queue positioning, the accounts map fills progressively down the Central Limit Order Book book. All accounts trade 20 contracts. Price immediately retraces 40 ticks against the position on MNQ, equivalent to a $2,000 loss on 20 contracts. The position sizing represents aggressive leverage for a $50,000 account, creating temporary open drawdown of 4% on the master account and 4.2-4.5% on slave accounts (due to worse fills). Under intraday trailing drawdown models, multiple slave accounts would breach the 5% threshold during this retracement, triggering immediate evaluation failure despite the eventual trade outcome. The master's 4% drawdown keeps it compliant, but worse-filled slave accounts blow. Under EOD drawdown calculation, this temporary variance becomes irrelevant. If price subsequently reverses and the trade closes profitably, all accounts close the day profitable with no drawdown violation. The intraday equity dip never triggers evaluation failure because the drawdown assessment occurs only against 5:00 PM closed equity. This creates a critical strategic advantage for copy trading operations: the ability to maintain aggressive position sizing (essential for reaching 10% profit targets efficiently) without the catastrophic failure risk that fill dispersion creates under intraday drawdown models.

The single-step 10% profit target, however, introduces a compensating difficulty. While two-step challenges (8% then 5%, typical at Top One Trader and E8 Futures) allow traders to demonstrate consistency across two separate evaluation periods, the single-step 10% challenge requires reaching a larger absolute target in one continuous evaluation phase. For a $50,000 account, this means generating $5,000 in profits while maintaining EOD equity above $47,500. If the account's highest equity point reaches $54,000, the 5% drawdown threshold doesn't trail—it remains static at $47,500 (5% below starting balance). This represents FundedNext's second major structural advantage: static maximum drawdown rather than trailing. The distinction is crucial: Trailing Drawdown models force the max loss threshold to follow peak equity, meaning an equity retrace can trigger a breach on a flat account. Static Drawdown models fix the max loss threshold to the starting balance. Account reaches $54,000, threshold stays $47,500. Equity can drop safely back down without breach. For profitable copy trading systems, static drawdowns provide vastly more operational latitude. After achieving $4,000 in profits, the strategy can endure a subsequent losing period without evaluation failure. This static structure particularly benefits volatile strategies with high win rates but occasional large losing periods—common characteristics of momentum and breakout systems. Under trailing drawdowns, a losing streak occurring immediately after a winning streak (when account equity peaked) triggers high breach risk. Under static drawdowns, the accumulated profits create a buffer against subsequent drawdowns.

FundedNext Futures offers evaluation account sizes from $15,000 to $200,000, with funded account scaling available up to $300,000 for top performers. The multi-account policy permits up to three funded accounts per trader identity simultaneously—a middle position between Goat Funded Futures (two accounts) and Top One Trader (four accounts). Three accounts at $200,000 each creates $600,000 total allocation potential—substantial capital for most retail systematic strategies, though half the ceiling of Top One Trader's maximum configuration. The profit split structure operates at 80% (trader) initially, increasing to 90% after the first profit withdrawal, and reaching 95% for accounts maintaining six months of profitability. This matches Top One Trader's senior-tier splits, making FundedNext competitive for long-term capital deployment. Platform connectivity focuses exclusively on Rithmic infrastructure. FundedNext does not currently support Tradovate or CQG integration, creating both a limitation (no protocol redundancy like E8 Futures) and an advantage (all accounts use identical connectivity infrastructure, minimizing latency variance across slave accounts). For copy trading operations, uniform Rithmic connectivity across all accounts simplifies technical architecture. The master and all slaves connect through the same protocol to the same data centers, eliminating protocol-specific latency variance. The tradeoff: no backup connectivity pathway during infrastructure outages.

Position limits during Flex Challenge evaluations permit 20 contracts on ES (80 MES, 15 NQ, 60 MNQ)—matching Goat Funded Futures and doubling E8 Futures' 10-contract evaluation limit. Post-funding, limits expand to 50 ES (200 MES, 35 NQ, 140 MNQ)—the most generous position limits among the four firms analyzed. For high-volume scalping strategies, these expanded limits create meaningful capacity advantages. A system designed to scale into positions across multiple entries can execute at full strategic scale on FundedNext funded accounts, while needing to reduce size on E8 Futures or Top One Trader accounts.

Section 3: Critical Technical Rules — Decoding Hidden Traps in Trade Copying

3.1 Multi-Account Limits: Structural Boundaries of Capital Aggregation

Summary Block: Futures prop firms implement multi-account ownership restrictions ranging from two concurrent funded accounts (Goat Funded Futures, E8 Futures) to four accounts (Top One Trader) per individual trader identity, with enforcement mechanisms tracking Social Security Numbers, IP addresses, hardware fingerprints, and trading pattern correlation analysis. Violating these limits through identity falsification constitutes contract breach triggering immediate account termination and profit forfeiture across all associated accounts.

The economic incentive to circumvent multi-account limits appears straightforward: if a prop firm permits two funded accounts but a trader wants to operate six, using additional identities (family members, business partners, purchased identities) could theoretically multiply capital access threefold. This approach violates every major prop firm's terms of service and creates catastrophic legal and financial risks.

The enforcement mechanisms operate across multiple technical layers: Identity Verification (KYC) requirements populating databases that cross-reference existing records; IP Address Geolocation Tracking that records session logs and catches sequential dynamic allocations within sequential subnets; Hardware Fingerprinting tracking MAC addresses, browser extensions, and unique device fingerprints; and Trading Pattern Correlation Analysis running automated surveillance algorithms. When correlation coefficients between two accounts' daily returns exceed 0.85 and show sub-second temporal synchronization, it triggers immediate contract breach. The legal and financial consequences create cascading losses: immediate platform bans, retroactive profit forfeiture, and inclusion on industry watchlists shared with clearing FCMs. Profitable traders must focus on fully compliant pathways: maximizing permitted allocations across firm diversification networks, structuring legitimate legal business entities, or utilizing direct performance-based corporate scaling tracks.

3.2 Trailing Drawdown vs. EOD Drawdown: Synchronization Failure Modes

Summary Block: Intraday trailing drawdown models monitor account equity tick-by-tick, triggering immediate evaluation failure when equity drops below maximum loss thresholds at any moment during market hours, creating zero tolerance for temporary fill dispersion inherent to copy trading. End-of-Day drawdown models evaluate compliance exclusively against closed equity at 5:00 PM Eastern, permitting temporary intraday equity fluctuations below static thresholds provided traders close positions to restore compliance before session close.

The temporal frequency of drawdown calculation creates fundamentally different risk environments for copy trading operations. Intraday Trailing Drawdown models (E8 Futures and Top One Trader) evaluate continuous equity checks every 100-200 milliseconds. As account equity peaks, the floor adjusts upward, transforming temporary unrealized gains into a permanent risk baseline. During high-velocity execution queue sequences, a 1-2 tick fill dispersion across synchronized slave accounts means minor intraday adverse movements create asymmetric breach failures on follower metrics, while the master account remains completely compliant. EOD Drawdown mechanics (FundedNext Futures and Goat Funded Futures) completely eliminate this failure mode by auditing risk metrics purely against 5:00 PM closed equity parameters. Intraday dips are entirely processed without contract violations, giving copy traders the operational latitude needed to sustain strategy exposure without worrying about infrastructure queue imperfections.

3.3 Prohibited Strategies: Enforcement Against Flipping, Grid Trading, and Latency Arbitrage

Summary Block: Futures prop firms universally prohibit "flipping" (opening opposing directional positions across multiple accounts simultaneously to guarantee profit on one account while accepting loss on others), grid trading systems (layering multiple limit orders at fixed price intervals), and latency arbitrage strategies exploiting feed delays. Detection algorithms analyze correlation coefficients across accounts, order placement patterns, and profitability distribution, triggering immediate termination and profit forfeiture upon identification.

The structural layout of prop challenges induces a mathematical asymmetry where traders are tempted to deploy exploitative mechanics rather than genuine market edge. Flipping strategies utilize opposing position configurations across synchronized identities to isolate profits on one account while offloading failure onto a decoupled setup. Surveillance algorithms flag these systems via inverse equity curve synchronization and multi-account correlation factors. Grid Trading environments place fixed-interval limits to harvest mean-reversion, but their massive overnight exposure and clearing bandwidth drain trigger immediate tracking blocks. Latency Arbitrage attempts to exploit delayed feed nodes on volatile economic seconds. Risk desks catch arb setups by measuring execution timestamps relative to Central Limit Order Book microsecond updates—resulting in direct retroactive profit denials across all reviewed entities.

3.4 IP Addresses & VPN Logs: KYC Compliance and Hardware Profiling

Summary Block: Futures prop firms implement multi-layered identity verification tracking IP address geolocation patterns, device hardware fingerprints, browser metadata, and login behavioral analysis to detect multi-account rule violations and identity falsification. VPN usage triggers enhanced scrutiny protocols, with consistent datacenter IP patterns flagging accounts for manual compliance review and potential enhanced documentation requirements before profit withdrawals.

Identity validation at modern clearing nodes goes beyond standard document scanning. Security systems continually screen for impossible geographic velocity (e.g., cross-continental authentication session overlap) and track commercial datacenter IP ranges. Exclusive routing through VPN nodes triggers strict compliance review gates, requiring physical utility bill cross-matching and deposit source trace audits. Legitimate trade copying operations must maintain uniform residential ISP connection paths or clear VPS datacenter IPs proactively with compliance desks prior to live execution. The single-identity profile must match across every integrated node to preserve uncompromised funded status.

Section 4: The Tech Stack — Setup and Optimization for Zero-Latency Copying

4.1 Execution Protocol Comparison: Tradovate vs. Rithmic vs. NinjaTrader

Summary Block: Rithmic R|Protocol delivers 8-15 millisecond order acknowledgment latency from submission to CME confirmation when servers colocate in Aurora data centers, representing the industry standard for institutional futures execution. Tradovate's cloud-native architecture introduces 25-45 millisecond baseline latency via AWS infrastructure intermediation, while NinjaTrader Continuum achieves 12-22 millisecond performance through proprietary CME connectivity, creating material performance variance for latency-sensitive copy trading strategies targeting sub-10-tick profit objectives.

The communication protocol linking trading platforms to CME exchange infrastructure determines the theoretical minimum execution latency. Rithmic Protocol operates via low-overhead binary formatting directly inside Chicago server centers, minimizing packet overhead and keeping round-trip latency within an elite 8-15ms envelope. Tradovate targets browser flexibility via WebSocket integrations running on Amazon Web Services clouds, introducing slight protocol serialization latency (24-71ms practical range) that can fluctuate during periods of regional cloud congestion. NinjaTrader Continuum delivers a highly optimized C# development layer built for NinjaScript executions, clocking a continuous 10-19ms framework. For high-volume copy operations running automated scalping modules, co-located Rithmic lines remain the gold standard to prevent fill divergence across follower nodes.

4.2 Local Software vs. Cloud API Bridging for Trade Replication

Summary Block: Local copy trading software (Quantower Order Cloning, NinjaTrader Multi-Account Manager) executes replication logic on trader-controlled hardware with direct simultaneous broker API connections, achieving 8-35 millisecond slave account triggering latency. Cloud-based bridging services introduce architectural intermediation requiring master account data transmission to remote servers, signal processing, and distribution to geographically dispersed slaves, compounding total replication latency to 85-220 milliseconds while creating single-point-of-failure dependency on third-party infrastructure uptime.

Selecting replication software defines your technical latency multiplier. Local cloning mechanisms (Quantower, Replikanto) maintain active concurrent TCP/IP connections from a single local environment, firing follower orders in absolute parallel within 8-35ms of master signal detection. Cloud bridging structures introduce remote cloud hops that add a fixed 85-220ms delay profile. For scalping systems running multi-account allocations, this structural variance compounds into catastrophic contract commission drain and slippage losses. Advanced portfolios resolve this drag by selecting automated mini-to-micro contract mapping via local engines, preserving proportional positioning while drastically flattening transaction friction profiles across smaller account limits.

Section 5: Radical Transparency Verdict

Winner: FundedNext Futures (Flex Challenge)

The definitive verdict for automated copy portfolios belongs to FundedNext's Flex Challenge. By providing exclusive EOD drawdown tracking, zero daily loss barriers, and stripping away funded consistency rules, it completely eliminates fill-dispersion breach risks. Automated EAs can compound capital efficiently across identical Tradovate and NinjaTrader API channels without artificial enforcement flags.

Winner: Goat Funded Futures ($50K EOD)

For capital-constrained systematic operations, Goat Funded Futures is the superior choice. Offering an elite entry price point for their $50K EOD model with zero minimum trading day restrictions, it empowers scalpers to secure funded credentials in a single active session, capitalizing on a 100% profit split on the first $10,000 to completely liquidate evaluation overhead.

Section 6: Frequently Asked Questions (High-Intent Q&A)

Is copy trading allowed across different futures prop firms?

Yes, personal copy trading between accounts registered under your own single identity is fully compliant across firms like Top One Trader and FundedNext. However, using external commercial signals or copy trading trades owned by another individual constitutes group trading and results in immediate account forfeiture.

Why does trailing drawdown crash copy trading portfolios?

Intraday trailing drawdown monitors account equity tick-by-tick. When a trade spikes into open profit, the drawdown floor moves up. If the price retraces back to breakeven, the follower accounts (which often experience execution slippage) lose that buffer permanently, creating a synchronization failure mode.

Which platform protocol is best for multi-account copy trading?

Rithmic R|Protocol is the absolute industry standard, delivering sub-15 millisecond execution latency when co-located in Chicago. Tradovate operates over cloud-native WebSockets on AWS, which introduces higher protocol overhead but provides better cross-account dashboard management.